IPPF

Internal auditors don't just follow rules, we have standards

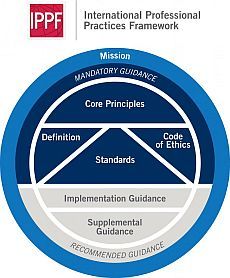

The mission for internal auditing is to enhance and protect organisational value by providing risk-based and objective assurance, advice and insight.

We rely on a framework of principles and standards to help us achieve this – the International Professional Practices Framework.

Mandatory guidance

Some elements of the IPPF are considered essential to the professional practice of internal auditing – they are mandatory for members of the Chartered IIA. Members agree to conform to these principles with they join the institute. The mandatory elements of the IPPF, which are explored in more depth below, are:

Definition of internal auditing

Core principles

Code of ethics

International Standards

1. Definition of internal auditing

Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organisation's operations. It helps an organisation accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes.

2. Core principles

The core principles articulate internal audit effectiveness and they should all be present and operating effectively.

- Demonstrates integrity.

- Demonstrates competence and due professional care.

- Is objective and free from undue influence (independent).

- Aligns with the strategies, objectives, and risks of the organisation.

- Is appropriately positioned and adequately resourced.

- Demonstrates quality and continuous improvement.

- Communicates effectively.

- Provides risk-based assurance.

- Is insightful, proactive, and future-focused.

- Promotes organisational improvement.

3. Code of ethics

The internal audit profession is founded on the trust placed in its objective assurance about risk management, control, and governance. The code of ethics provides principles and rules of conduct relating to integrity, objectivity, confidentiality and competency.

Read more about the code of ethics

4. International Standards

The International Standards is an authoritative set of guidance consisting of statements of basic requirements for the practice of internal audit and interpretations that clarify terms or concepts within those statements. The Standards were last updated on 1 January 2017.

The structure of the Standards is divided between attribute and performance standards:

- Attribute standards address the attributes of organisations and individuals performing internal auditing.

- Performance standards describe the nature of internal auditing and provide quality criteria against which the performance of these services can be measured.

Recommended guidance

The IPPF also includes guidance to help internal auditors implement the Standards and apply best practice to all internal audit work. This forms the 'recommended' element of the framework.

Two kinds of guidance are produced:

1. Implementation guidance

Implementation guides help internal auditors apply the Standards. They collectively address internal auditing's approach, methodologies, and consideration, but do not detail processes or procedures.

2. Supplemental guidance

Supplemental guidance describes processes and procedures in detail as well as sector specific issues and topical areas. These guides will help you develop the tools, techniques and programmes you need with a step-by-step approach. Supplemental guidance will also help you to determine what the deliverables are.